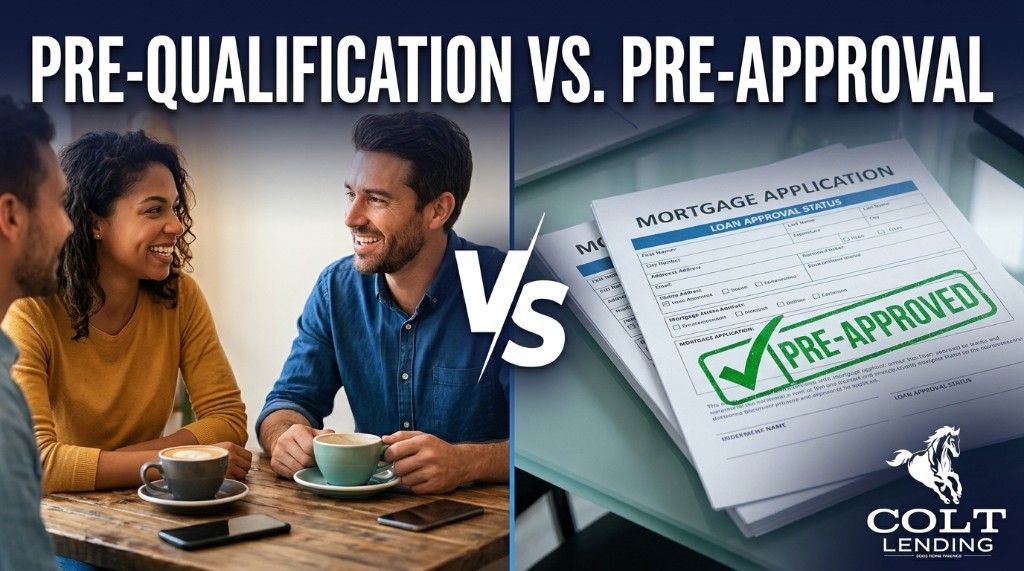

Everyone in real estate talks about getting pre-approved like it's a magic stamp that means you're good to go.

Your realtor wants it. Sellers want it. Every mortgage website says it's step one.

But here's what most people are not told: the name on the letter - whether it says pre-qualification or pre-approval - often matters less than the work behind it.

I've seen pre-approval letters generated in minutes with minimal analysis. I have also seen pre-qualification letters backed by real scenario testing, guideline review, and lender matching that survive underwriting cleanly.

The label does not tell you much. The process behind the letter tells you everything.

Why This Distinction Exists

In Texas, institutions lending their own money (banks, credit unions, direct lenders) issue formal pre-approvals. Mortgage brokers, who originate through wholesale lenders, issue pre-qualification letters.

That naming convention is legal and structural. It does not inherently measure strength, depth, or closeability.

As a broker, I shop your scenario across a large lender network rather than forcing your profile into one institution's box. In many real-world files, that creates a stronger outcome.

What Goes Into a Strong Pre-Qualification

I am not just running a credit pull and accepting one automated result.

I test your scenario across multiple lenders. Different lenders can treat the same borrower differently based on overlays, appetite, and risk interpretation.

If a borrower has non-standard income, prior credit events, or timeline complexity, one lender may decline while another approves with clear conditions.

The difference between denied and approved is often lender fit, not borrower quality.

I also use direct lender support channels and account executives to validate edge-case guidelines before a letter is issued, so we are not guessing after you go under contract.

By the time a strong pre-qualification letter is issued, potential risk points are identified and we already have a plan to navigate them.

What Happens in Many Retail Workflows

Not every retail lender operates the same way, but many borrowers experience a narrow process:

One product shelf.

One overlay profile.

Limited flexibility when your scenario is not standard.

When the only available answer is one institution's answer, borrowers can miss approvals and pricing available elsewhere.

Lender Overlays: The Hidden Variable

Agency guidelines (Fannie Mae, Freddie Mac, FHA, VA, USDA) define baseline eligibility.

Lenders then add overlays, which are stricter internal rules layered on top.

Examples:

One lender requires a higher credit score than agency minimums.

Another caps DTI lower than automated approval findings.

Another applies tighter restrictions to gift funds or property type.

A broker pre-qualification should account for both agency rules and lender overlays, then align you with lenders where your scenario is strongest.

What You Should Actually Evaluate

Forget the label and evaluate the quality of the process:

How many lenders were checked?

Were potential issues surfaced before you write an offer?

Can your mortgage professional explain exactly why and where you qualify?

Do they have resources for complex files when surprises appear?

The strongest letter is not the one with the fanciest name. It is the one backed by the best work.

The Bigger Picture

Consumers are often trained to ask for a pre-approval letter without being shown how much quality can vary between letters.

A quick one-lender letter and a market-tested multi-lender letter are not equivalent, even if the names suggest otherwise.

The name on the letter does not close your loan. The work behind it does.

Ready to See Where You Actually Stand?

If you want a thorough qualification strategy, I can run your scenario, shop it across my lender network, and map out the most reliable path to closing.

Start with the Homebuyer Readiness Quiz, or schedule a call and we will walk through your numbers together.